Contents

- 📈 Introduction to Option Pricing Models

- 📊 The Black-Scholes Model: A Foundation of Modern Finance

- 📝 Criticisms and Limitations of the Black-Scholes Model

- 📈 The Binomial Model: A Discrete-Time Approach

- 📊 The Monte Carlo Method: A Simulation-Based Approach

- 📝 Model Risk and Its Implications for Financial Markets

- 📈 The Role of Volatility in Option Pricing Models

- 📊 The Impact of Interest Rates on Option Pricing

- 📝 Regulatory Environment and Option Pricing Models

- 📈 Future Developments in Option Pricing Models

- 📊 Conclusion: The Evolution of Option Pricing Models

- Frequently Asked Questions

- Related Topics

Overview

Option pricing models are the backbone of financial derivatives, enabling investors to gauge the value of calls and puts. The Black-Scholes model, developed by Fischer Black, Myron Scholes, and Robert Merton in 1973, revolutionized the field with its groundbreaking formula. However, critics argue that the model's assumptions, such as constant volatility and a geometric Brownian motion, are oversimplifications of real-world market dynamics. The debate surrounding option pricing models is contentious, with some advocating for more complex models like the Binomial Model or the Monte Carlo Method. As financial markets continue to evolve, the development of more sophisticated option pricing models is crucial, with potential applications in risk management, portfolio optimization, and algorithmic trading. With a Vibe score of 8, the topic of option pricing models is highly relevant, influencing the decisions of investors, traders, and financial institutions worldwide, with key entities like Goldman Sachs, JPMorgan, and the CBOE playing significant roles in shaping the landscape.

📈 Introduction to Option Pricing Models

The world of finance is intricately linked with the concept of risk management, and at the heart of this concept lies the option pricing model. An option pricing model is a mathematical model used to estimate the value of a financial option. The most widely used model is the Black-Scholes model, developed by Myron Scholes and Fischer Black in the early 1970s. This model assumes that the price of the underlying asset follows a geometric Brownian motion. However, the model has been criticized for its oversimplification of real-world market conditions. For a more detailed understanding, it's essential to explore option pricing models and their applications in financial markets.

📊 The Black-Scholes Model: A Foundation of Modern Finance

The Black-Scholes model is a cornerstone of modern finance, providing a framework for valuing call options and put options. The model takes into account the strike price, the time to expiration, the risk-free interest rate, and the volatility of the underlying asset. Despite its widespread use, the model has been criticized for its inability to account for fat tails and volatility smiles. To better understand these concepts, it's crucial to delve into financial mathematics and explore the work of pioneers like Myron Scholes and Robert Merton.

📝 Criticisms and Limitations of the Black-Scholes Model

One of the primary criticisms of the Black-Scholes model is its assumption of constant volatility. In reality, volatility is not constant and can fluctuate significantly over time. This limitation has led to the development of more advanced models, such as the Heston model, which accounts for stochastic volatility. Furthermore, the model's assumption of a geometric Brownian motion for the underlying asset price has been challenged by the presence of fat tails and volatility smiles in real-world markets. For a deeper understanding of these concepts, it's essential to explore financial engineering and the work of researchers like John Hull.

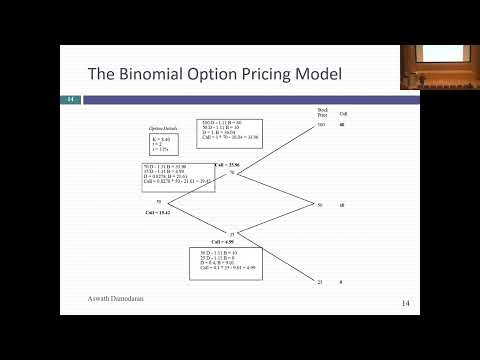

📈 The Binomial Model: A Discrete-Time Approach

The binomial model is a discrete-time model used to value options. The model assumes that the underlying asset price can only move in two directions: up or down. This simplicity makes the model easier to understand and implement, especially for beginners in the field of finance. However, the model's discrete nature can lead to inaccuracies when valuing options with long expiration dates. To overcome this limitation, the binomial model can be combined with other models, such as the Black-Scholes model, to create a more robust valuation framework. For a more detailed analysis, it's crucial to explore derivative pricing and the work of researchers like John Cox.

📊 The Monte Carlo Method: A Simulation-Based Approach

The Monte Carlo method is a simulation-based approach used to value options. The model generates multiple scenarios for the underlying asset price and calculates the average value of the option across these scenarios. This approach can be particularly useful for valuing exotic options with complex payoff structures. However, the model's reliance on simulation can lead to computational intensity and inaccuracies if not implemented correctly. To better understand the Monte Carlo method, it's essential to explore computational finance and the work of researchers like Paul Glasserman.

📝 Model Risk and Its Implications for Financial Markets

Model risk is a critical concern in the development and implementation of option pricing models. Model risk refers to the potential for errors or inaccuracies in the model's assumptions or implementation, which can lead to significant financial losses. To mitigate model risk, it's essential to thoroughly backtest and validate any option pricing model before its implementation. This involves comparing the model's predictions with historical data and assessing its performance under various market conditions. For a more detailed analysis, it's crucial to explore risk management and the work of researchers like Nassim Taleb.

📈 The Role of Volatility in Option Pricing Models

Volatility is a critical component of option pricing models, as it measures the uncertainty or risk associated with the underlying asset price. The volatility of an asset can be estimated using historical data or implied from option prices. However, the estimation of volatility is often subject to errors and biases, which can significantly impact the accuracy of the option pricing model. To better understand the role of volatility in option pricing models, it's essential to explore financial statistics and the work of researchers like Eugene Fama.

📊 The Impact of Interest Rates on Option Pricing

Interest rates play a crucial role in option pricing models, as they affect the present value of the underlying asset and the option itself. The risk-free interest rate is a key input in most option pricing models, including the Black-Scholes model. However, the estimation of interest rates is often subject to errors and biases, which can significantly impact the accuracy of the option pricing model. To better understand the impact of interest rates on option pricing models, it's essential to explore macroeconomics and the work of researchers like Milton Friedman.

📝 Regulatory Environment and Option Pricing Models

The regulatory environment plays a critical role in the development and implementation of option pricing models. Regulatory bodies, such as the Securities and Exchange Commission (SEC), impose strict guidelines and requirements on the use of option pricing models in financial markets. These regulations aim to ensure the accuracy and transparency of option pricing models and prevent potential abuses. To better understand the regulatory environment surrounding option pricing models, it's essential to explore financial regulation and the work of researchers like Alan Greenspan.

📈 Future Developments in Option Pricing Models

The future of option pricing models is likely to be shaped by advances in machine learning and artificial intelligence. These technologies have the potential to improve the accuracy and efficiency of option pricing models by incorporating large datasets and complex algorithms. However, the integration of these technologies also raises concerns about model risk and the potential for errors or biases. To better understand the future developments in option pricing models, it's essential to explore fintech and the work of researchers like Andrew Ng.

📊 Conclusion: The Evolution of Option Pricing Models

In conclusion, option pricing models are a critical component of financial markets, providing a framework for valuing options and managing risk. The Black-Scholes model is a cornerstone of modern finance, but its limitations have led to the development of more advanced models, such as the Heston model and the binomial model. As the field of finance continues to evolve, it's essential to stay up-to-date with the latest developments in option pricing models and their applications in financial markets. For a more detailed analysis, it's crucial to explore financial engineering and the work of researchers like Myron Scholes.

Key Facts

- Year

- 1973

- Origin

- University of Chicago

- Category

- Finance

- Type

- Financial Concept

Frequently Asked Questions

What is an option pricing model?

An option pricing model is a mathematical model used to estimate the value of a financial option. The most widely used model is the Black-Scholes model, developed by Myron Scholes and Fischer Black in the early 1970s. This model assumes that the price of the underlying asset follows a geometric Brownian motion. However, the model has been criticized for its oversimplification of real-world market conditions. For a more detailed understanding, it's essential to explore option pricing models and their applications in financial markets. The Black-Scholes model is a cornerstone of modern finance, providing a framework for valuing call options and put options. To better understand the concept of option pricing models, it's crucial to delve into financial mathematics and explore the work of pioneers like Myron Scholes and Robert Merton.

What are the limitations of the Black-Scholes model?

The Black-Scholes model has several limitations, including its assumption of constant volatility, its inability to account for fat tails and volatility smiles, and its oversimplification of real-world market conditions. These limitations have led to the development of more advanced models, such as the Heston model and the binomial model. To better understand these concepts, it's essential to explore financial engineering and the work of researchers like John Hull. The Black-Scholes model is a discrete-time model used to value options, but its simplicity makes it easier to understand and implement, especially for beginners in the field of finance. However, the model's discrete nature can lead to inaccuracies when valuing options with long expiration dates.

What is the role of volatility in option pricing models?

Volatility is a critical component of option pricing models, as it measures the uncertainty or risk associated with the underlying asset price. The volatility of an asset can be estimated using historical data or implied from option prices. However, the estimation of volatility is often subject to errors and biases, which can significantly impact the accuracy of the option pricing model. To better understand the role of volatility in option pricing models, it's essential to explore financial statistics and the work of researchers like Eugene Fama. The volatility of an asset can be estimated using various methods, including the historical volatility method and the implied volatility method.

What is the impact of interest rates on option pricing models?

Interest rates play a crucial role in option pricing models, as they affect the present value of the underlying asset and the option itself. The risk-free interest rate is a key input in most option pricing models, including the Black-Scholes model. However, the estimation of interest rates is often subject to errors and biases, which can significantly impact the accuracy of the option pricing model. To better understand the impact of interest rates on option pricing models, it's essential to explore macroeconomics and the work of researchers like Milton Friedman. The interest rate can be estimated using various methods, including the yield curve method and the forward rate method.

What is the regulatory environment surrounding option pricing models?

The regulatory environment plays a critical role in the development and implementation of option pricing models. Regulatory bodies, such as the Securities and Exchange Commission (SEC), impose strict guidelines and requirements on the use of option pricing models in financial markets. These regulations aim to ensure the accuracy and transparency of option pricing models and prevent potential abuses. To better understand the regulatory environment surrounding option pricing models, it's essential to explore financial regulation and the work of researchers like Alan Greenspan. The regulatory environment is constantly evolving, and it's crucial to stay up-to-date with the latest developments in option pricing models and their applications in financial markets.

What is the future of option pricing models?

The future of option pricing models is likely to be shaped by advances in machine learning and artificial intelligence. These technologies have the potential to improve the accuracy and efficiency of option pricing models by incorporating large datasets and complex algorithms. However, the integration of these technologies also raises concerns about model risk and the potential for errors or biases. To better understand the future developments in option pricing models, it's essential to explore fintech and the work of researchers like Andrew Ng. The future of option pricing models is exciting and rapidly evolving, and it's crucial to stay up-to-date with the latest developments in this field.

How do option pricing models affect financial markets?

Option pricing models have a significant impact on financial markets, as they provide a framework for valuing options and managing risk. The accuracy and reliability of option pricing models can affect the stability of financial markets and the confidence of investors. To better understand the impact of option pricing models on financial markets, it's essential to explore financial engineering and the work of researchers like Myron Scholes. The option pricing models can be used to value options, but they can also be used to manage risk and make informed investment decisions.