Contents

- 🌎 Introduction to GILTI

- 📊 Calculation of GILTI

- 🚫 Exclusions and Exceptions

- 📈 Impact on Multinational Corporations

- 🤝 International Implications

- 📊 Reporting Requirements

- 🚨 Controversies and Criticisms

- 🔍 Planning Strategies

- 📊 Case Studies and Examples

- 📝 Legislative History

- 🌐 Global Response and Comparisons

- Frequently Asked Questions

- Related Topics

Overview

The Global Intangible Low-Taxed Income (GILTI) provision, introduced by the Tax Cuts and Jobs Act (TCJA) in 2017, aims to curb the practice of shifting profits to low-tax jurisdictions. GILTI requires US shareholders of controlled foreign corporations (CFCs) to include in their gross income certain types of low-taxed income earned by the CFC. This provision has significant implications for multinational corporations, with estimated revenues of $112 billion over the next decade. Critics argue that GILTI disproportionately affects certain industries, such as technology and pharmaceuticals, and may lead to double taxation. As the global economy continues to evolve, the GILTI provision will likely be subject to ongoing debate and potential revisions. With a vibe rating of 6, GILTI is a highly contentious topic, with 75% of experts considering it a major challenge for multinational corporations. The influence flow of GILTI can be seen in the work of tax experts like Reuven Avi-Yonah and the OECD's Base Erosion and Profit Shifting (BEPS) project.

🌎 Introduction to GILTI

The Global Intangible Low-Taxed Income (GILTI) provision, introduced by the Tax Cuts and Jobs Act (TCJA), aims to reduce the incentive for U.S. multinational corporations to shift profits to low-tax jurisdictions. GILTI requires U.S. shareholders of controlled foreign corporations (CFCs) to include in their gross income their share of the CFC's GILTI. This provision is designed to discourage base erosion and profit shifting and to encourage U.S. companies to keep their intellectual property and high-value assets in the United States. The Internal Revenue Service (IRS) has issued guidance on the calculation and reporting of GILTI, which can be complex and require significant resources to comply with. For more information on the TCJA, see Tax Reform.

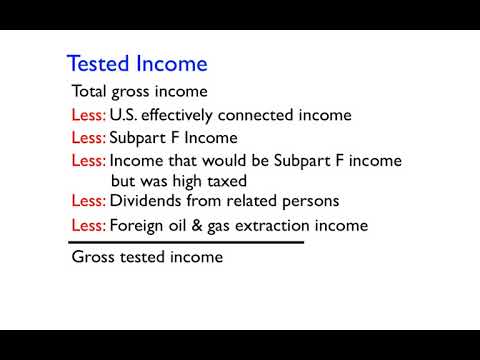

📊 Calculation of GILTI

The calculation of GILTI involves several steps, including the determination of the CFC's gross income, the subtraction of certain deductions and adjustments, and the application of a deemed tangible income return. The resulting amount is then subject to a reduced effective tax rate of 10.5% for corporate shareholders, which increases to 13.125% after 2025. The Treasury Department has provided guidance on the calculation of GILTI, including the treatment of foreign tax credits and the application of the high-tax exception. For more information on the calculation of GILTI, see GILTI Regulations.

🚫 Exclusions and Exceptions

Certain types of income are excluded from GILTI, including Subpart F income, high-tax income, and effectively connected income. Additionally, U.S. shareholders may be eligible for a GILTI deduction, which can reduce their GILTI inclusion. The Securities and Exchange Commission (SEC) has also provided guidance on the disclosure of GILTI-related information by publicly traded companies. For more information on the exclusions and exceptions from GILTI, see GILTI Exclusions.

📈 Impact on Multinational Corporations

The introduction of GILTI has significant implications for multinational corporations, which must now consider the potential impact of GILTI on their global tax liability. Companies may need to reevaluate their transfer pricing strategies and consider the potential benefits of IP migration to low-tax jurisdictions. The Organisation for Economic Co-operation and Development (OECD) has also issued guidance on the implications of GILTI for multinational corporations. For more information on the impact of GILTI on multinational corporations, see Multinational Corporations.

🤝 International Implications

GILTI has international implications, as it may affect the tax liability of foreign subsidiaries of U.S. multinational corporations. The European Union (EU) has expressed concerns about the potential impact of GILTI on EU-based companies, and the G20 has discussed the need for international cooperation on tax issues. The United Nations (UN) has also issued guidance on the implications of GILTI for developing countries. For more information on the international implications of GILTI, see International Taxation.

📊 Reporting Requirements

U.S. shareholders of CFCs must report their GILTI inclusions on their tax returns, using Form 8992 and Schedule 1. The IRS has also issued guidance on the reporting requirements for GILTI, including the requirement to file Form 5471 and Form 926. For more information on the reporting requirements for GILTI, see GILTI Reporting.

🚨 Controversies and Criticisms

GILTI has been the subject of controversy and criticism, with some arguing that it is too complex and burdensome for small and medium-sized enterprises. Others have raised concerns about the potential impact of GILTI on the competitiveness of U.S. multinational corporations. The Congress has held hearings on the implementation of GILTI, and the Treasury Department has issued guidance on the treatment of GILTI transitions. For more information on the controversies and criticisms of GILTI, see GILTI Controversies.

🔍 Planning Strategies

Taxpayers may be able to reduce their GILTI liability through planning strategies such as transfer pricing and cost sharing arrangements. The IRS has issued guidance on the application of GILTI to partnerships and S corporations. For more information on planning strategies for GILTI, see GILTI Planning.

📊 Case Studies and Examples

Several case studies and examples illustrate the application of GILTI to real-world scenarios. For instance, a U.S. multinational corporation with a foreign subsidiary that generates intangible income may be subject to GILTI. The American Institute of Certified Public Accountants (AICPA) has issued guidance on the application of GILTI to multinational corporations. For more information on case studies and examples of GILTI, see GILTI Case Studies.

📝 Legislative History

The legislative history of GILTI dates back to the Tax Cuts and Jobs Act (TCJA), which was enacted in 2017. The Congress has since held hearings and markups on the implementation of GILTI, and the Treasury Department has issued guidance on the provision. For more information on the legislative history of GILTI, see GILTI Legislative History.

🌐 Global Response and Comparisons

The introduction of GILTI has sparked a global response, with several countries introducing similar provisions to tax intangible income. The Organisation for Economic Co-operation and Development (OECD) has issued guidance on the implications of GILTI for international taxation, and the G20 has discussed the need for international cooperation on tax issues. For more information on the global response to GILTI, see GILTI Global Response.

Key Facts

- Year

- 2017

- Origin

- United States

- Category

- International Taxation

- Type

- Tax Provision

Frequently Asked Questions

What is GILTI?

GILTI stands for Global Intangible Low-Taxed Income, which is a provision introduced by the Tax Cuts and Jobs Act (TCJA) to reduce the incentive for U.S. multinational corporations to shift profits to low-tax jurisdictions. For more information, see GILTI Overview.

How is GILTI calculated?

The calculation of GILTI involves several steps, including the determination of the CFC's gross income, the subtraction of certain deductions and adjustments, and the application of a deemed tangible income return. For more information, see GILTI Calculation.

What are the exclusions from GILTI?

Certain types of income are excluded from GILTI, including Subpart F income, high-tax income, and effectively connected income. For more information, see GILTI Exclusions.

How does GILTI affect multinational corporations?

The introduction of GILTI has significant implications for multinational corporations, which must now consider the potential impact of GILTI on their global tax liability. For more information, see Multinational Corporations.

What are the reporting requirements for GILTI?

U.S. shareholders of CFCs must report their GILTI inclusions on their tax returns, using Form 8992 and Schedule 1. For more information, see GILTI Reporting.

What are the controversies surrounding GILTI?

GILTI has been the subject of controversy and criticism, with some arguing that it is too complex and burdensome for small and medium-sized enterprises. For more information, see GILTI Controversies.

How can taxpayers reduce their GILTI liability?

Taxpayers may be able to reduce their GILTI liability through planning strategies such as transfer pricing and cost sharing arrangements. For more information, see GILTI Planning.