Contents

Overview

Duration risk refers to the sensitivity of a bond's price to changes in interest rates, with higher duration bonds being more vulnerable to rate fluctuations. This risk is a major concern for investors with fixed-income portfolios, as rising interest rates can lead to significant losses. According to a study by the Federal Reserve, a 1% increase in interest rates can result in a 9% decline in the value of a 10-year bond with a duration of 8 years. The concept of duration was first introduced by economist Frederick Macaulay in 1938, and since then, it has become a crucial tool for investors to manage their risk exposure. With the current low-interest-rate environment, investors are particularly vulnerable to duration risk, with some estimates suggesting that a 1% increase in rates could lead to losses of up to $1.4 trillion in the US bond market alone. As the global economy continues to evolve, understanding duration risk will be essential for investors to navigate the complexities of the fixed-income market.

📊 Introduction to Duration Risk

Duration risk is a critical concept in fixed-income investing, referring to the sensitivity of a bond's price to changes in interest rates. As explained in Fixed Income Investing, bonds with longer durations are more sensitive to interest rate changes. This is because Interest Rates have a greater impact on the present value of future cash flows for longer-term bonds. The Bond Market is particularly vulnerable to duration risk, as changes in interest rates can significantly affect bond prices. To mitigate this risk, investors often use Duration Matching strategies. Additionally, understanding Yield Curve dynamics is essential for managing duration risk.

📈 Understanding Duration and Its Impact

The duration of a bond is a measure of its sensitivity to changes in interest rates, and it is typically calculated using the Macaulay Duration formula. This formula takes into account the bond's Coupon Rate, Time to Maturity, and Yield to Maturity. As discussed in Bond Valuation, the duration of a bond is a key factor in determining its price volatility. Investors can use Bond Ladders to manage duration risk and reduce the impact of interest rate changes on their portfolios. Furthermore, Interest Rate Derivatives can be used to hedge against duration risk. The Efficient Market Hypothesis suggests that bond prices reflect all available information, including interest rate expectations.

📊 Measuring Duration Risk

Measuring duration risk is crucial for fixed-income investors, as it helps them understand the potential impact of interest rate changes on their portfolios. The Duration-Based Approach involves calculating the duration of each bond in the portfolio and then aggregating the results to determine the overall duration risk. This approach is often used in conjunction with Value at Risk models to estimate the potential loss of a portfolio due to interest rate changes. Investors can also use Stress Testing to evaluate the resilience of their portfolios to different interest rate scenarios. As noted in Risk Management, measuring duration risk is an essential step in developing an effective risk management strategy. Additionally, Scenario Analysis can be used to evaluate the potential impact of different interest rate scenarios on a portfolio.

📈 Managing Duration Risk

Managing duration risk is essential for fixed-income investors, as it can help them reduce the impact of interest rate changes on their portfolios. One approach is to use Liability-Driven Investing strategies, which involve matching the duration of the portfolio to the duration of the liabilities. This approach can help investors reduce the risk of unexpected losses due to interest rate changes. Another approach is to use Duration Matching strategies, which involve matching the duration of the portfolio to the desired level of risk. As noted in Portfolio Management, managing duration risk is an ongoing process that requires continuous monitoring and adjustment. Investors can also use ETFs to gain exposure to different bond markets and manage duration risk. Additionally, Mutual Funds can provide a diversified portfolio with a targeted duration profile.

📊 Interest Rate Risk and Duration

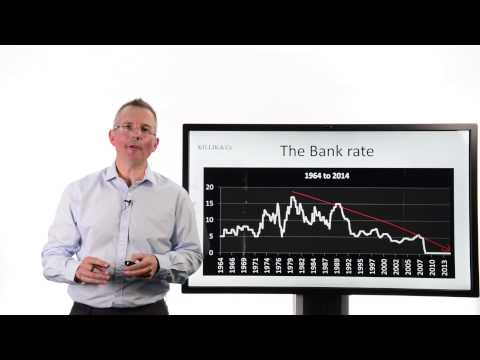

Interest rate risk is a key component of duration risk, as changes in interest rates can have a significant impact on bond prices. As explained in Interest Rate Risk, interest rate changes can affect the present value of future cash flows, leading to changes in bond prices. The Yield Curve is a key indicator of interest rate expectations, and changes in the yield curve can have a significant impact on bond prices. Investors can use Interest Rate Derivatives to hedge against interest rate risk and reduce the impact of interest rate changes on their portfolios. Furthermore, Bond Futures can be used to manage interest rate risk and gain exposure to different bond markets. The Federal Reserve plays a critical role in setting interest rates and shaping the yield curve.

📈 Credit Risk and Duration

Credit risk is another important consideration when managing duration risk, as changes in credit spreads can affect bond prices. As discussed in Credit Risk, credit spreads reflect the market's perception of the issuer's creditworthiness, and changes in credit spreads can have a significant impact on bond prices. The Credit Default Swap market is a key indicator of credit risk, and changes in credit default swap spreads can have a significant impact on bond prices. Investors can use Credit Derivatives to hedge against credit risk and reduce the impact of credit spread changes on their portfolios. Additionally, Collateralized Loan Obligations can be used to manage credit risk and gain exposure to different credit markets. The Basel III regulatory framework has introduced new requirements for managing credit risk in banking institutions.

In conclusion, duration risk is a critical consideration for fixed-income investors, as it can have a significant impact on bond prices and portfolio returns. By understanding the concepts of duration and interest rate risk, investors can develop effective strategies for managing duration risk and reducing the impact of interest rate changes on their portfolios. As noted in Investing, managing duration risk is an ongoing process that requires continuous monitoring and adjustment. Investors can use a range of tools and strategies, including Duration Matching, Liability-Driven Investing, and Interest Rate Derivatives, to manage duration risk and achieve their investment objectives. The VIX Index is often used as a benchmark for measuring market volatility and managing risk.

Key Facts

- Year

- 1938

- Origin

- Frederick Macaulay

- Category

- Finance

- Type

- Financial Concept

Frequently Asked Questions

What is duration risk?

Duration risk refers to the sensitivity of a bond's price to changes in interest rates. It is a critical concept in fixed-income investing, as changes in interest rates can have a significant impact on bond prices and portfolio returns. As explained in Fixed Income Investing, bonds with longer durations are more sensitive to interest rate changes. The Bond Market is particularly vulnerable to duration risk, as changes in interest rates can significantly affect bond prices.

How is duration calculated?

Duration is typically calculated using the Macaulay Duration formula, which takes into account the bond's Coupon Rate, Time to Maturity, and Yield to Maturity. This formula provides a measure of the bond's sensitivity to changes in interest rates. As discussed in Bond Valuation, the duration of a bond is a key factor in determining its price volatility. Investors can use Bond Ladders to manage duration risk and reduce the impact of interest rate changes on their portfolios.

What is the difference between duration risk and interest rate risk?

Duration risk and interest rate risk are related but distinct concepts. Duration risk refers to the sensitivity of a bond's price to changes in interest rates, while interest rate risk refers to the potential impact of interest rate changes on a portfolio's value. As explained in Interest Rate Risk, interest rate changes can affect the present value of future cash flows, leading to changes in bond prices. The Yield Curve is a key indicator of interest rate expectations, and changes in the yield curve can have a significant impact on bond prices.

How can investors manage duration risk?

Investors can manage duration risk by using a range of strategies, including Duration Matching, Liability-Driven Investing, and Interest Rate Derivatives. These strategies can help investors reduce the impact of interest rate changes on their portfolios and achieve their investment objectives. As noted in Portfolio Management, managing duration risk is an ongoing process that requires continuous monitoring and adjustment. Investors can also use ETFs to gain exposure to different bond markets and manage duration risk.

What is the role of credit risk in duration risk management?

Credit risk is an important consideration when managing duration risk, as changes in credit spreads can affect bond prices. As discussed in Credit Risk, credit spreads reflect the market's perception of the issuer's creditworthiness, and changes in credit spreads can have a significant impact on bond prices. The Credit Default Swap market is a key indicator of credit risk, and changes in credit default swap spreads can have a significant impact on bond prices. Investors can use Credit Derivatives to hedge against credit risk and reduce the impact of credit spread changes on their portfolios.