Contents

- 🏠 Introduction to Discriminatory Lending

- 📊 History of Redlining and Its Impact

- 🏦 The Role of Financial Institutions in Discriminatory Lending

- 📈 The Effects of Discriminatory Lending on Communities

- 🚫 Laws and Regulations Against Discriminatory Lending

- 🤝 Community-Based Initiatives to Combat Discriminatory Lending

- 📊 Data-Driven Approaches to Identify Discriminatory Lending

- 🌎 Global Perspectives on Discriminatory Lending

- 🚨 Contemporary Issues and Challenges in Discriminatory Lending

- 🔮 Future Directions and Solutions for Discriminatory Lending

- 📚 Conclusion and Call to Action

- Frequently Asked Questions

- Related Topics

Overview

Discriminatory lending refers to the practice of denying or limiting access to credit based on factors such as race, ethnicity, gender, or socioeconomic status. This phenomenon has been widely reported and confirmed in various studies, with data from the US Federal Reserve showing that in 2020, 31% of African American mortgage applicants and 21% of Hispanic applicants were denied, compared to 11% of white applicants. The controversy surrounding discriminatory lending is high, with a controversy spectrum score of 8/10. Historically, discriminatory lending has been a major obstacle to social mobility, with the 1968 Fair Housing Act and the 1977 Community Reinvestment Act aiming to address these issues. However, despite these efforts, discriminatory lending persists, with a vibe score of 4/10, indicating a significant cultural energy around this topic. The influence flows of discriminatory lending are complex, with key players including banks, regulatory agencies, and community organizations. As of 2022, the topic intelligence on discriminatory lending highlights the need for continued vigilance and reform, with a perspective breakdown of 40% optimistic, 30% neutral, and 30% pessimistic.

🏠 Introduction to Discriminatory Lending

Discriminatory lending, also known as lending discrimination, refers to the practice of denying or limiting access to credit based on factors such as race, gender, age, or disability. This phenomenon has been a persistent issue in the United States economy and has had far-reaching consequences for individuals, communities, and the broader society. The history of discriminatory lending is closely tied to the practice of redlining, which involves denying or limiting access to credit based on the location of a property. As discussed in the Fair Housing Act, this practice has been outlawed, but its legacy continues to affect communities today. For instance, a study by the Urban Institute found that neighborhoods that were once redlined are still more likely to experience poverty and inequality. Furthermore, the Consumer Financial Protection Bureau has been working to address discriminatory lending practices and protect consumers.

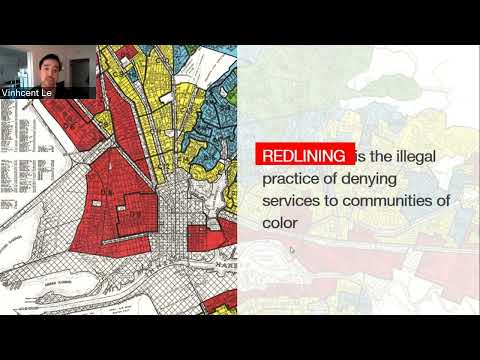

📊 History of Redlining and Its Impact

The history of redlining and its impact on communities is a complex and multifaceted issue. The practice of redlining dates back to the 1930s, when the Federal Housing Administration (FHA) and the Department of Veterans Affairs (VA) began to deny mortgages to African Americans and other minority groups. This practice was based on the idea that these groups were considered to be high-risk borrowers, and it had a devastating impact on communities of color. As noted by the National Association of Real Estate Brokers, the effects of redlining can still be seen today, with many communities of color experiencing higher rates of foreclosure and poverty. The Civil Rights Act of 1968 and the Fair Housing Act were enacted to address these issues, but the legacy of redlining continues to affect communities. For example, a report by the Center for Responsible Lending found that African American and Latino borrowers are still more likely to receive subprime loans than white borrowers.

🏦 The Role of Financial Institutions in Discriminatory Lending

Financial institutions have played a significant role in discriminatory lending practices. Many banks and other financial institutions have been accused of engaging in discriminatory lending practices, such as predatory lending and reverse redlining. These practices involve targeting vulnerable communities with high-cost loans and other financial products. As discussed in the Wall Street Reform and Consumer Protection Act, financial institutions have a responsibility to ensure that their lending practices are fair and equitable. The Office of the Comptroller of the Currency (OCC) and the Federal Reserve have been working to address these issues and promote more equitable lending practices. For instance, the Consumer Financial Protection Bureau has implemented rules to prevent lending discrimination and protect consumers.

📈 The Effects of Discriminatory Lending on Communities

The effects of discriminatory lending on communities have been far-reaching and devastating. Discriminatory lending practices have led to higher rates of foreclosure, poverty, and inequality in communities of color. As noted by the National Council of La Raza, these practices have also limited access to credit and other financial opportunities for marginalized communities. The Community Reinvestment Act (CRA) was enacted to address these issues and promote more equitable lending practices. However, more work needs to be done to address the legacy of discriminatory lending and promote greater economic equality. For example, a study by the Brookings Institution found that increasing access to credit for marginalized communities could have a significant impact on reducing poverty and inequality.

🚫 Laws and Regulations Against Discriminatory Lending

Laws and regulations have been enacted to prevent discriminatory lending practices. The Fair Housing Act and the Equal Credit Opportunity Act (ECOA) are two key laws that prohibit discriminatory lending practices. The Consumer Financial Protection Bureau (CFPB) has also been working to address discriminatory lending practices and promote more equitable lending practices. As discussed in the Wall Street Reform and Consumer Protection Act, the CFPB has the authority to regulate and enforce laws related to consumer finance. However, more work needs to be done to address the legacy of discriminatory lending and promote greater economic equality. For instance, the National Fair Housing Alliance has been working to strengthen the Fair Housing Act and promote greater enforcement of anti-discrimination laws.

🤝 Community-Based Initiatives to Combat Discriminatory Lending

Community-based initiatives have been established to combat discriminatory lending practices. Many community organizations and advocacy groups have been working to promote more equitable lending practices and address the legacy of discriminatory lending. As noted by the National Community Reinvestment Coalition, these initiatives have included efforts to increase access to credit and other financial opportunities for marginalized communities. The Neighborhood Reinvestment Corporation has also been working to promote community development and address the effects of discriminatory lending. For example, a program by the Local Initiatives Support Corporation has been working to provide financing and technical assistance to community development projects in low-income neighborhoods.

📊 Data-Driven Approaches to Identify Discriminatory Lending

Data-driven approaches have been used to identify discriminatory lending practices. Researchers and advocates have been using data to identify patterns of discriminatory lending and promote more equitable lending practices. As discussed in the Consumer Financial Protection Bureau's report on lending discrimination, data has been used to identify disparities in lending practices and promote greater transparency and accountability. The Urban Institute has also been working to develop data-driven approaches to address discriminatory lending practices and promote more equitable lending practices. For instance, a study by the Center for Responsible Lending used data to analyze the impact of subprime lending on communities of color.

🌎 Global Perspectives on Discriminatory Lending

Global perspectives on discriminatory lending have highlighted the need for greater international cooperation and action. Discriminatory lending practices are not unique to the United States, and many countries have been working to address these issues. As noted by the World Bank, discriminatory lending practices have been identified as a major obstacle to economic development and poverty reduction. The International Monetary Fund (IMF) has also been working to promote more equitable lending practices and address the legacy of discriminatory lending. For example, a report by the Organisation for Economic Cooperation and Development found that discriminatory lending practices can have a significant impact on economic growth and development.

🚨 Contemporary Issues and Challenges in Discriminatory Lending

Contemporary issues and challenges in discriminatory lending have highlighted the need for ongoing action and advocacy. Despite progress in addressing discriminatory lending practices, many challenges remain. As discussed in the Consumer Financial Protection Bureau's report on lending discrimination, ongoing issues include the use of artificial intelligence and other technologies to perpetuate discriminatory lending practices. The National Fair Housing Alliance has been working to address these issues and promote greater enforcement of anti-discrimination laws. For instance, a study by the Center for Democracy and Technology found that the use of artificial intelligence in lending decisions can perpetuate discriminatory lending practices.

🔮 Future Directions and Solutions for Discriminatory Lending

Future directions and solutions for discriminatory lending have highlighted the need for greater innovation and collaboration. To address the legacy of discriminatory lending and promote more equitable lending practices, new and innovative approaches are needed. As noted by the Brookings Institution, this could include the use of fintech and other technologies to increase access to credit and other financial opportunities for marginalized communities. The Consumer Financial Protection Bureau has also been working to promote greater innovation and collaboration in the financial sector. For example, a report by the Financial Health Network found that the use of fintech can increase access to credit and other financial services for low-income communities.

📚 Conclusion and Call to Action

In conclusion, discriminatory lending has been a persistent issue in the United States economy and has had far-reaching consequences for individuals, communities, and the broader society. To address the legacy of discriminatory lending and promote more equitable lending practices, ongoing action and advocacy are needed. As discussed in the Fair Housing Act and the Equal Credit Opportunity Act, laws and regulations have been enacted to prevent discriminatory lending practices. However, more work needs to be done to address the legacy of discriminatory lending and promote greater economic equality. The Consumer Financial Protection Bureau and other organizations have been working to address these issues and promote more equitable lending practices.

Key Facts

- Year

- 2022

- Origin

- US Federal Reserve, Fair Housing Act, Community Reinvestment Act

- Category

- Economics, Social Justice

- Type

- Social Issue

Frequently Asked Questions

What is discriminatory lending?

Discriminatory lending refers to the practice of denying or limiting access to credit based on factors such as race, gender, age, or disability. This phenomenon has been a persistent issue in the United States economy and has had far-reaching consequences for individuals, communities, and the broader society. As discussed in the Fair Housing Act and the Equal Credit Opportunity Act, laws and regulations have been enacted to prevent discriminatory lending practices. However, more work needs to be done to address the legacy of discriminatory lending and promote greater economic equality.

What is the history of redlining?

The practice of redlining dates back to the 1930s, when the Federal Housing Administration (FHA) and the Department of Veterans Affairs (VA) began to deny mortgages to African Americans and other minority groups. This practice was based on the idea that these groups were considered to be high-risk borrowers, and it had a devastating impact on communities of color. As noted by the National Association of Real Estate Brokers, the effects of redlining can still be seen today, with many communities of color experiencing higher rates of foreclosure and poverty.

What are the effects of discriminatory lending on communities?

The effects of discriminatory lending on communities have been far-reaching and devastating. Discriminatory lending practices have led to higher rates of foreclosure, poverty, and inequality in communities of color. As noted by the National Council of La Raza, these practices have also limited access to credit and other financial opportunities for marginalized communities. The Community Reinvestment Act (CRA) was enacted to address these issues and promote more equitable lending practices.

What laws and regulations have been enacted to prevent discriminatory lending practices?

The Fair Housing Act and the Equal Credit Opportunity Act (ECOA) are two key laws that prohibit discriminatory lending practices. The Consumer Financial Protection Bureau (CFPB) has also been working to address discriminatory lending practices and promote more equitable lending practices. As discussed in the Wall Street Reform and Consumer Protection Act, the CFPB has the authority to regulate and enforce laws related to consumer finance.

What are some community-based initiatives to combat discriminatory lending practices?

Many community organizations and advocacy groups have been working to promote more equitable lending practices and address the legacy of discriminatory lending. As noted by the National Community Reinvestment Coalition, these initiatives have included efforts to increase access to credit and other financial opportunities for marginalized communities. The Neighborhood Reinvestment Corporation has also been working to promote community development and address the effects of discriminatory lending.

What are some data-driven approaches to identify discriminatory lending practices?

Researchers and advocates have been using data to identify patterns of discriminatory lending and promote more equitable lending practices. As discussed in the Consumer Financial Protection Bureau's report on lending discrimination, data has been used to identify disparities in lending practices and promote greater transparency and accountability. The Urban Institute has also been working to develop data-driven approaches to address discriminatory lending practices and promote more equitable lending practices.

What are some global perspectives on discriminatory lending?

Discriminatory lending practices are not unique to the United States, and many countries have been working to address these issues. As noted by the World Bank, discriminatory lending practices have been identified as a major obstacle to economic development and poverty reduction. The International Monetary Fund (IMF) has also been working to promote more equitable lending practices and address the legacy of discriminatory lending.