Contents

- 📊 Introduction to Annual Percentage Rate (APR)

- 💸 Understanding Nominal APR and Effective APR

- 📈 How APR Works: A Breakdown

- 📊 Calculating APR: The Formula

- 🚨 The Hidden Costs of Borrowing: APR in Practice

- 🤝 Comparing APRs: A Key to Informed Decision-Making

- 📊 APR Regulation: Protecting Consumers

- 📈 The Future of APR: Trends and Insights

- 📊 Case Studies: Real-World Examples of APR

- 📝 Conclusion: Navigating the World of APR

- Frequently Asked Questions

- Related Topics

Overview

The Annual Percentage Rate (APR) is a crucial concept in personal finance, representing the total cost of borrowing, including interest rates and fees. Introduced by the Truth in Lending Act of 1968, APR aims to provide transparency and standardization in lending practices. However, critics argue that APR can be misleading, as it does not account for compounding interest and other factors. With a Vibe score of 60, APR is a widely discussed topic, sparking debates among economists, policymakers, and consumers. According to a report by the Consumer Financial Protection Bureau (CFPB), the average APR for credit cards in the US is around 16.4%. As the financial landscape continues to evolve, understanding APR is essential for making informed decisions about borrowing and managing debt. The concept of APR has been influenced by key figures such as Senator Paul Douglas, who sponsored the Truth in Lending Act, and has been shaped by various events, including the 2008 financial crisis.

📊 Introduction to Annual Percentage Rate (APR)

The Annual Percentage Rate (APR) is a crucial concept in the world of finance, particularly when it comes to borrowing money. As defined by the Finance industry, APR is the interest rate for a whole year, rather than just a monthly fee/rate, as applied on a loan, mortgage loan, credit card, etc. It is a finance charge expressed as an annual rate, which can be either a Nominal APR or an Effective APR (EAPR). The nominal APR is the simple-interest rate, while the effective APR is the fee+compound interest rate. To understand APR, it's essential to explore its history and development, including the role of Central Banks in regulating interest rates.

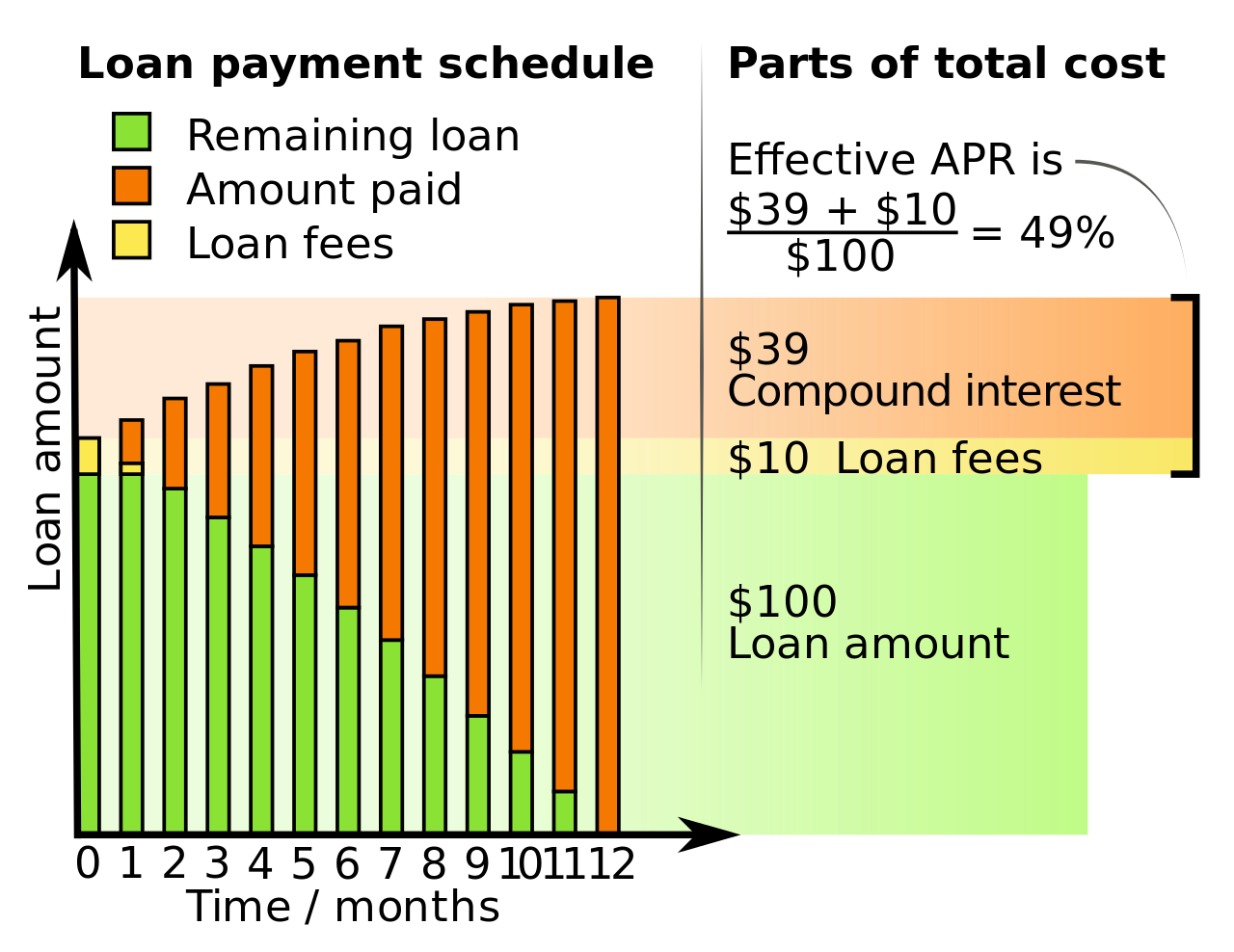

💸 Understanding Nominal APR and Effective APR

When it comes to understanding APR, it's vital to distinguish between the nominal APR and the effective APR. The nominal APR is the simple-interest rate, which is the rate at which interest is calculated on a loan or credit product. On the other hand, the effective APR takes into account the compounding of interest, which can result in a higher overall cost. For example, a credit card with a nominal APR of 20% might have an effective APR of 25% or more, depending on the compounding frequency. This is why it's essential to consider the Credit Score and Interest Rates when applying for a loan or credit product.

📈 How APR Works: A Breakdown

So, how does APR work in practice? Let's consider a scenario where an individual takes out a personal loan with a nominal APR of 15%. If the loan is for $10,000 and the borrower repays it over 5 years, the total interest paid will be $4,347. However, if the effective APR is 18% due to compounding, the total interest paid will be $5,419. This highlights the importance of understanding the difference between nominal and effective APR, as well as the role of Compound Interest in calculating the total cost of borrowing. Additionally, borrowers should be aware of the Loan Terms and conditions before signing any agreement.

📊 Calculating APR: The Formula

Calculating APR can be a complex process, but it's essential to understand the formula. The APR formula takes into account the interest rate, fees, and compounding frequency to calculate the effective APR. For example, if a credit card has a nominal APR of 20% and a fee of $50 per year, the effective APR will be higher than the nominal APR. The formula for calculating APR is: APR = (1 + (interest rate/number of periods))^number of periods - 1. This formula can be applied to various financial products, including Mortgage Loans and Credit Cards.

🤝 Comparing APRs: A Key to Informed Decision-Making

Comparing APRs is a key part of making informed decisions when borrowing money. By comparing the APRs of different loan products, individuals can determine which option is the most cost-effective. For example, a personal loan with an APR of 12% might seem like a good deal, but if a credit card has an APR of 10% and a 0% introductory offer, it might be a better option. This is why it's essential to consider the Credit Limit and Interest-Free Period when comparing different financial products. Additionally, borrowers should be aware of the Balance Transfer options available to them.

📊 APR Regulation: Protecting Consumers

APR regulation is an essential aspect of protecting consumers from predatory lending practices. In the United States, the Truth in Lending Act (TILA) requires lenders to disclose the APR and other terms of a loan or credit product. This regulation helps to ensure that consumers have access to clear and accurate information when making decisions about borrowing money. However, there are still many challenges in regulating APR, particularly in the context of Fintech and Online Lending.

📈 The Future of APR: Trends and Insights

The future of APR is likely to be shaped by trends such as Digitalization and Sustainability. As more financial products become available online, it's likely that APR will become more transparent and competitive. Additionally, there may be a greater emphasis on sustainable lending practices, which could lead to the development of new APR models that take into account environmental and social factors. This is why it's essential to stay up-to-date with the latest developments in the Financial Technology sector.

📊 Case Studies: Real-World Examples of APR

Case studies can provide valuable insights into the real-world implications of APR. For example, a study of mortgage borrowers found that those who understood the APR and other terms of their loan were more likely to make informed decisions and avoid costly mistakes. Another study found that credit card borrowers who were aware of the APR and fees associated with their card were more likely to pay off their balance in full each month. These studies highlight the importance of Financial Literacy and Consumer Protection in the context of APR.

Key Facts

- Year

- 1968

- Origin

- United States

- Category

- Finance

- Type

- Financial Concept

Frequently Asked Questions

What is the difference between nominal APR and effective APR?

The nominal APR is the simple-interest rate, while the effective APR takes into account the compounding of interest. The effective APR is typically higher than the nominal APR and provides a more accurate picture of the total cost of borrowing. For example, a credit card with a nominal APR of 20% might have an effective APR of 25% or more, depending on the compounding frequency. This is why it's essential to consider the Credit Score and Interest Rates when applying for a loan or credit product.

How is APR calculated?

The APR formula takes into account the interest rate, fees, and compounding frequency to calculate the effective APR. The formula is: APR = (1 + (interest rate/number of periods))^number of periods - 1. This formula can be applied to various financial products, including Mortgage Loans and Credit Cards.

What is the importance of understanding APR?

Understanding APR is crucial when borrowing money, as it helps individuals make informed decisions about the total cost of the loan. By considering the APR and other terms of a loan or credit product, individuals can avoid costly mistakes and make more informed decisions. This is why it's essential to consult with a Financial Advisor and stay informed about the latest developments in the Financial Markets.

How does APR regulation protect consumers?

APR regulation, such as the Truth in Lending Act (TILA), requires lenders to disclose the APR and other terms of a loan or credit product. This regulation helps to ensure that consumers have access to clear and accurate information when making decisions about borrowing money. However, there are still many challenges in regulating APR, particularly in the context of Fintech and Online Lending.

What are the future trends in APR?

The future of APR is likely to be shaped by trends such as Digitalization and Sustainability. As more financial products become available online, it's likely that APR will become more transparent and competitive. Additionally, there may be a greater emphasis on sustainable lending practices, which could lead to the development of new APR models that take into account environmental and social factors.